Introduction

The Constitution Amendment Bill on Goods and Services Tax (GST) has

received Presidential assent post its passage in both the houses of Parliament

and ratification by over one-half of the State Legislatures. The GST Council,

headed by the Union Finance Minister with all the State Finance Ministers as

members, is in the process of finalizing and recommending model GST law and

allied rules, rate of tax, threshold limits, exemptions, dispute resolution

mechanism, etc. Based on the recommendations of the GST Council, the

Parliament would pass two Bills for levy of Central GST and Integrated GST by

the Central Government and each of the State Legislatures would pass a Bill for

levy of State GST.

For successful implementation of GST, necessary Information Technology (IT)

infrastructure is required to be put in place by the Government for ensuring

smooth transition from the existing indirect tax structure into the GST regime.

The portal being developed by Goods and Services Tax Network (GSTN) will

act as a common interface between tax payers, tax authorities, banks and the

Reserve Bank of India for exchange of information. While the GSTN is working

relentlessly to ensure that the above authorities get the best of IT infrastructure

for efficient administration of GST, the Government is also progressing promptly

by imparting GST training of its officials at the Central and States. The

Government also intends to kick start Vyapak Abhiyan towards the end of

the year to bring awareness about GST among the public at large.

The burden now shifts on to the taxpayers to assess their level of preparedness

in studying the impact of the new law to their transactions and analyze if their IT

infrastructure matches the compliance requirements of the new regime. The

GST proposes to create a common national market by reducing the cascading

effect of tax on the cost of goods and services. It therefore calls for a change in

the tax functions (including tax structure, tax computation, tax payment, tax

incidence, credit availment and utilization) of existing businesses. It will also

have an impact on other functions of the organization such as IT, Finance,

Marketing, Supply chain, Legal, etc. It is therefore imperative for us to introspect

where we stand and how well we are prepared to comply with the provisions of

the proposed GST law. In this article, we intend to throw some light on the

compliance requirements in filing of various returns and broad concepts of

matching of input tax credit, based on the information presently available in public domain.

The Constitution Amendment Bill on Goods and Services Tax (GST) has

received Presidential assent post its passage in both the houses of Parliament

and ratification by over one-half of the State Legislatures. The GST Council,

headed by the Union Finance Minister with all the State Finance Ministers as

members, is in the process of finalizing and recommending model GST law and

allied rules, rate of tax, threshold limits, exemptions, dispute resolution

mechanism, etc. Based on the recommendations of the GST Council, the

Parliament would pass two Bills for levy of Central GST and Integrated GST by

the Central Government and each of the State Legislatures would pass a Bill for

levy of State GST.

For successful implementation of GST, necessary Information Technology (IT)

infrastructure is required to be put in place by the Government for ensuring

smooth transition from the existing indirect tax structure into the GST regime.

The portal being developed by Goods and Services Tax Network (GSTN) will

act as a common interface between tax payers, tax authorities, banks and the

Reserve Bank of India for exchange of information. While the GSTN is working

relentlessly to ensure that the above authorities get the best of IT infrastructure

for efficient administration of GST, the Government is also progressing promptly

by imparting GST training of its officials at the Central and States. The

Government also intends to kick start Vyapak Abhiyan towards the end of

the year to bring awareness about GST among the public at large.

The burden now shifts on to the taxpayers to assess their level of preparedness

in studying the impact of the new law to their transactions and analyze if their IT

infrastructure matches the compliance requirements of the new regime. The

GST proposes to create a common national market by reducing the cascading

effect of tax on the cost of goods and services. It therefore calls for a change in

the tax functions (including tax structure, tax computation, tax payment, tax

incidence, credit availment and utilization) of existing businesses. It will also

have an impact on other functions of the organization such as IT, Finance,

Marketing, Supply chain, Legal, etc. It is therefore imperative for us to introspect

where we stand and how well we are prepared to comply with the provisions of

the proposed GST law. In this article, we intend to throw some light on the

compliance requirements in filing of various returns and broad concepts of

matching of input tax credit, based on the information presently available in public domain.

Basic overview on GST Returns

While all the returns under GST would be required to be filed electronically, the

details of Central and State taxes would be consolidated together for the

purpose of reporting the details of outward and inward supplies, Input Tax

Credits (ITC), tax payments, etc. A normal registered taxable person is required

to file two basic forms in a month, namely GSTR-1 and GSTR-2. These forms

represent details of outward supplies and inward supplies of goods and services

effected in a particular tax period. A normal registered taxable person is also

required to file a return in form GSTR-3 on a monthly basis, consolidating the

details of outward and inward supplies, ITC availed, Tax payable, Tax paid and

other particulars.

While all the returns under GST would be required to be filed electronically, the

details of Central and State taxes would be consolidated together for the

purpose of reporting the details of outward and inward supplies, Input Tax

Credits (ITC), tax payments, etc. A normal registered taxable person is required

to file two basic forms in a month, namely GSTR-1 and GSTR-2. These forms

represent details of outward supplies and inward supplies of goods and services

effected in a particular tax period. A normal registered taxable person is also

required to file a return in form GSTR-3 on a monthly basis, consolidating the

details of outward and inward supplies, ITC availed, Tax payable, Tax paid and

other particulars.

In addition to the above returns, a registered taxable person is also required to file

an Annual Return in form GSTR-9 (not GSTR-8, as provided under the report of the

Joint Committee on business process on GST Return, in October 2015). Specific

provisions have been made for filing the First Return by every assessee. Further,

returns have also been prescribed for followings –

1 – Composition taxpayer (in form GSTR-4)

2 – Non-resident foreign taxpayer (in form GSTR-5)

3 – Input Service Distributor (in form GSTR-6)

4 – TDS deductor (in form GSTR-7).

A registered taxable person is also required to file a Final Return in case of

cancellation of registration. There is no provision for revising the returns, but

rectification of errors/omissions is allowed upto a prescribed time period. It may be

noted that levy for late fee for delay or non-filing of returns are prescribed.

Outward and Inward Supply

Outward supplies include details relating to zero-rated supplies, inter-state supplies,

return of goods received in relation to/in pursuance of an inward supply, exports,

debit notes, credit notes and supplementary invoices. The details of outward

supplies for a tax period must be filed on or before 10th day of the month

succeeding such tax period, in form GSTR-1. The model law contemplates that the

details of each of the outward supply made during a month must be communicated

to the recipient within a specified timeframe. In our view, the communication to the

recipient would be routed through GSTN as such the details would be autopopulated

in the concerned tables of GSTR-2 of the recipient. No rectification can

be carried out in form GSTR-1 after filing form GSTR-3 for the month of September

of the subsequent financial year (FY) or after filing form GSTR-9, whichever is

earlier.

A normal registered taxable person is required to verify, validate, modify or delete

details relating to his inward supplies. He may also provide details of his inward

supplies received by him, which have not been declared by supplier in his Return.

He must furnish details of inward supplies of taxable goods/services, including

inward supply of services on which tax is payable on reverse charge and inward

supply of goods/services taxable under the IGST Act, received during a tax period

on or before 15th day of the month succeeding such tax period in form GSTR-2. Just

like form GSTR-1, no rectification can be carried out in form GSTR-2 after filing

form GSTR-3 for the month of September of the subsequent FY or after filing form

GSTR-9, whichever is earlier.

An assessee is required to enter invoice level details for each of his transactions.Entering invoice level details is necessary for reconciliation of tax deposits and endto-

end reconciliation of ITC. Invoice level detailing would also help the Government

in determining the share of tax attributable to destination state in case of an interstate

supply. This is going to be a cumbersome process for both small and large

scale dealers. Small assessee may find it difficult to manually enter the details of

invoices month on month and large assessee may face infrastructural bottleneck in

uploading huge volume of data. The industry has raised some concern on the

reconciliation of ITC at invoice level detail, calling it cumbersome and impractical.

However, in my view, in order to ensure compliance at all levels of the supply chain,

and to eradicate evasion of tax and fraudulent transactions, the requirement of

entering invoice level details would be imperative and worth the effort.

an Annual Return in form GSTR-9 (not GSTR-8, as provided under the report of the

Joint Committee on business process on GST Return, in October 2015). Specific

provisions have been made for filing the First Return by every assessee. Further,

returns have also been prescribed for followings –

1 – Composition taxpayer (in form GSTR-4)

2 – Non-resident foreign taxpayer (in form GSTR-5)

3 – Input Service Distributor (in form GSTR-6)

4 – TDS deductor (in form GSTR-7).

A registered taxable person is also required to file a Final Return in case of

cancellation of registration. There is no provision for revising the returns, but

rectification of errors/omissions is allowed upto a prescribed time period. It may be

noted that levy for late fee for delay or non-filing of returns are prescribed.

Outward and Inward Supply

Outward supplies include details relating to zero-rated supplies, inter-state supplies,

return of goods received in relation to/in pursuance of an inward supply, exports,

debit notes, credit notes and supplementary invoices. The details of outward

supplies for a tax period must be filed on or before 10th day of the month

succeeding such tax period, in form GSTR-1. The model law contemplates that the

details of each of the outward supply made during a month must be communicated

to the recipient within a specified timeframe. In our view, the communication to the

recipient would be routed through GSTN as such the details would be autopopulated

in the concerned tables of GSTR-2 of the recipient. No rectification can

be carried out in form GSTR-1 after filing form GSTR-3 for the month of September

of the subsequent financial year (FY) or after filing form GSTR-9, whichever is

earlier.

A normal registered taxable person is required to verify, validate, modify or delete

details relating to his inward supplies. He may also provide details of his inward

supplies received by him, which have not been declared by supplier in his Return.

He must furnish details of inward supplies of taxable goods/services, including

inward supply of services on which tax is payable on reverse charge and inward

supply of goods/services taxable under the IGST Act, received during a tax period

on or before 15th day of the month succeeding such tax period in form GSTR-2. Just

like form GSTR-1, no rectification can be carried out in form GSTR-2 after filing

form GSTR-3 for the month of September of the subsequent FY or after filing form

GSTR-9, whichever is earlier.

An assessee is required to enter invoice level details for each of his transactions.Entering invoice level details is necessary for reconciliation of tax deposits and endto-

end reconciliation of ITC. Invoice level detailing would also help the Government

in determining the share of tax attributable to destination state in case of an interstate

supply. This is going to be a cumbersome process for both small and large

scale dealers. Small assessee may find it difficult to manually enter the details of

invoices month on month and large assessee may face infrastructural bottleneck in

uploading huge volume of data. The industry has raised some concern on the

reconciliation of ITC at invoice level detail, calling it cumbersome and impractical.

However, in my view, in order to ensure compliance at all levels of the supply chain,

and to eradicate evasion of tax and fraudulent transactions, the requirement of

entering invoice level details would be imperative and worth the effort.

Consolidated Return GSTR – 3

A consolidated return in form GSTR-3 providing details of inward and outward

supplies of goods/services, ITC availed, Tax payable, Tax paid and other relevant

particulars are required to be filed by registered taxable person on or before 20th

day of the succeeding month. A registered taxable person shall not be allowed to

furnish form GSTR-3 for a tax period if valid return for any previous tax period has

not been furnished by him. It may be noted that the tax for the relevant tax period

should be paid on or before the due date of filing of form GSTR-3. Furnishing of

GSTR-3 without payment of full tax due as per such return shall not be treated as a

valid return for allowing ITC in respect of supplies made by such person. The

consequences of such conditional provision for allowing ITC are discussed in

greater detail in later part of this article, under ITC matching.

Filing of GSTR-3 on monthly basis is mandatory whether or not any supplies of

goods/services have been effected during such month. No rectification can be

carried out in form GSTR-3 after due date of filing form GSTR-3 for the month of

September or 2nd quarter of the subsequent FY or after filing form GSTR 8,

whichever is earlier. A Composition taxpayer must furnish form GSTR-4 for each

quarter or part thereof within 18 days after the end of each quarter. An ISD must

furnish form GSTR-6 within 13 days after the end of the month. A registered taxable

person deducting tax at source must furnish form GSTR-7 and pay tax so deducted

within 10 days after the end of the month.

A consolidated return in form GSTR-3 providing details of inward and outward

supplies of goods/services, ITC availed, Tax payable, Tax paid and other relevant

particulars are required to be filed by registered taxable person on or before 20th

day of the succeeding month. A registered taxable person shall not be allowed to

furnish form GSTR-3 for a tax period if valid return for any previous tax period has

not been furnished by him. It may be noted that the tax for the relevant tax period

should be paid on or before the due date of filing of form GSTR-3. Furnishing of

GSTR-3 without payment of full tax due as per such return shall not be treated as a

valid return for allowing ITC in respect of supplies made by such person. The

consequences of such conditional provision for allowing ITC are discussed in

greater detail in later part of this article, under ITC matching.

Filing of GSTR-3 on monthly basis is mandatory whether or not any supplies of

goods/services have been effected during such month. No rectification can be

carried out in form GSTR-3 after due date of filing form GSTR-3 for the month of

September or 2nd quarter of the subsequent FY or after filing form GSTR 8,

whichever is earlier. A Composition taxpayer must furnish form GSTR-4 for each

quarter or part thereof within 18 days after the end of each quarter. An ISD must

furnish form GSTR-6 within 13 days after the end of the month. A registered taxable

person deducting tax at source must furnish form GSTR-7 and pay tax so deducted

within 10 days after the end of the month.

Annual Return GSTR – 9

Form GSTR-9 is required to be furnished by every registered taxable person, other

than ISD, TDS deductor, Casual taxable person and Non-resident taxable person

on or before 31st December following the end of the FY. Persons required to get

their accounts audited must also furnish annual return along with audited copy of

annual accounts and reconciliation statement, reconciling the value of supplies

declared in annual return with annual financial statement.

The Model GST law contemplates that a taxable person cannot take the credit of

tax paid on goods and/or services after filing GSTR-3 for the month of September

following the end of financial year to which such invoice pertains or filing of the

relevant Annual Return (31st December), whichever is earlier.

than ISD, TDS deductor, Casual taxable person and Non-resident taxable person

on or before 31st December following the end of the FY. Persons required to get

their accounts audited must also furnish annual return along with audited copy of

annual accounts and reconciliation statement, reconciling the value of supplies

declared in annual return with annual financial statement.

The Model GST law contemplates that a taxable person cannot take the credit of

tax paid on goods and/or services after filing GSTR-3 for the month of September

following the end of financial year to which such invoice pertains or filing of the

relevant Annual Return (31st December), whichever is earlier.

First and Final Return

The concept of filing a First Return and Final Return have been newly introduced.

These returns play an important role of providing details of the assessee at the time

of entry into and exit from the GSTN. The First return is required to be furnished by

every registered taxable person on whom the levy of GST applies. It contemplates

for providing the details of:

(a) outward supplies from the date on which he became liable to registration till the

end of the month in which the registration is granted, and

(b) inward supplies from the effective date of registration till the end of the month in

which the registration is granted.

A Composition taxpayer is required to furnish the First Return for the period starting

from the date on which he becomes a registered taxable person till the end of the

quarter in which the registration is granted. Every registered taxable person

applying for cancellation of registration shall furnish a Final Return within 3 months

of the date of cancellation or date of cancellation order, whichever is later.The

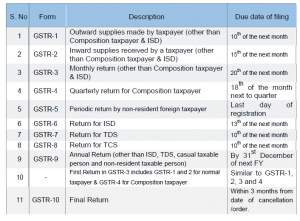

compliance schedule for filing of returns under GST can be summarized in the form

of a table as under:

These returns play an important role of providing details of the assessee at the time

of entry into and exit from the GSTN. The First return is required to be furnished by

every registered taxable person on whom the levy of GST applies. It contemplates

for providing the details of:

(a) outward supplies from the date on which he became liable to registration till the

end of the month in which the registration is granted, and

(b) inward supplies from the effective date of registration till the end of the month in

which the registration is granted.

A Composition taxpayer is required to furnish the First Return for the period starting

from the date on which he becomes a registered taxable person till the end of the

quarter in which the registration is granted. Every registered taxable person

applying for cancellation of registration shall furnish a Final Return within 3 months

of the date of cancellation or date of cancellation order, whichever is later.The

compliance schedule for filing of returns under GST can be summarized in the form

of a table as under:

Penal Provisions Relating to Returns

If a registered taxable person fails to furnish form GSTR-9 or Final Return, he

shall be served with a notice requiring him to furnish such the Return within a

statutory timeframe. Any registered taxable person who fails to furnish form

GSTR-1, GSTR-2, GSTR-3 or Final Return within the due dates, shall be liable

to pay a late fee of Rs. 100 per day during which such failure continues, subject

to maximum of Rs. 5,000. Similarly, any registered taxable person who fails to

furnish form GSTR-9 within the due date, shall be liable to a late fee of Rs. 100

per day during which such failure continues, subject to maximum of an amount

calculated @ 0.25% of his aggregate turnover.

Matching, Reversal and Reclaim of ITC

The concept of matching of ITC may not be new to the taxpayers, especially for

the dealers who are currently operating under the Value Added Tax (VAT)

regime. However, the same is alien or relatively new to non-VAT taxpayers and

hence there is a need to understand the concepts of ITC matching, ITC

reversals and re-claim of ITC in GST regime.

Before discussing the concept of ITC matching, it is imperative to understand

the concept of Debit Notes in GST regime, as it has a bearing on reclaim of ITC.

The Model GST law provides that:

Debit note can be issued by a taxable person who has supplied goods

and/or services (Issue of Debit note by the recipient is not contemplated

under GST regime).

Debit note can be issued when the value and/or tax as shown in the tax

invoice is less than the taxable value and/or tax in respect of supply of

goods and/or services.

The taxable person must already have issued tax invoice for supply of

goods and/or services by indicating the taxable value and/or tax on the tax

invoice.

Essentially, Debit Notes can be issued by the Supplier to the Recipient for

differential portion of the value or tax or both. Having understood the basic

aspects of Debit Note, let us move ahead to examine and understand the

concepts of ITC matching and its related topics.

If a registered taxable person fails to furnish form GSTR-9 or Final Return, he

shall be served with a notice requiring him to furnish such the Return within a

statutory timeframe. Any registered taxable person who fails to furnish form

GSTR-1, GSTR-2, GSTR-3 or Final Return within the due dates, shall be liable

to pay a late fee of Rs. 100 per day during which such failure continues, subject

to maximum of Rs. 5,000. Similarly, any registered taxable person who fails to

furnish form GSTR-9 within the due date, shall be liable to a late fee of Rs. 100

per day during which such failure continues, subject to maximum of an amount

calculated @ 0.25% of his aggregate turnover.

Matching, Reversal and Reclaim of ITC

The concept of matching of ITC may not be new to the taxpayers, especially for

the dealers who are currently operating under the Value Added Tax (VAT)

regime. However, the same is alien or relatively new to non-VAT taxpayers and

hence there is a need to understand the concepts of ITC matching, ITC

reversals and re-claim of ITC in GST regime.

Before discussing the concept of ITC matching, it is imperative to understand

the concept of Debit Notes in GST regime, as it has a bearing on reclaim of ITC.

The Model GST law provides that:

Debit note can be issued by a taxable person who has supplied goods

and/or services (Issue of Debit note by the recipient is not contemplated

under GST regime).

Debit note can be issued when the value and/or tax as shown in the tax

invoice is less than the taxable value and/or tax in respect of supply of

goods and/or services.

The taxable person must already have issued tax invoice for supply of

goods and/or services by indicating the taxable value and/or tax on the tax

invoice.

Essentially, Debit Notes can be issued by the Supplier to the Recipient for

differential portion of the value or tax or both. Having understood the basic

aspects of Debit Note, let us move ahead to examine and understand the

concepts of ITC matching and its related topics.

ITC Matching

On a broader analysis of the Report of Joint Committee on Business Process

for GST on GST Returns read along with the Model GST law, the matching,

reversal and reclaim of ITC can largely be understood as a fool proof

mechanism to tap revenue leakage in the hands of the Government. In order to

check for duplication of claim of ITC, the details of every inward supply

furnished by the taxable person (i.e. the “recipient” of goods and/or services) in

form GSTR-2 shall be matched:

With the corresponding details of outward supply furnished by the

corresponding taxable person (i.e. the “supplier” of goods and / or services)

in his valid return for the same tax period or any preceding tax period and

With the additional duty of customs i.e. IGST paid by the recipient in respect

of goods imported.

Therefore, the quintessential requirement for carrying out matching of ITC is

that the supplier must have filed his valid returns for the corresponding or

preceding tax period and/or the IGST has been paid by the recipient in case of

import of goods.

Failure to file valid return by the Supplier (or failure to pay appropriate IGST by

the recipient in case of import of goods) may lead to denial of ITC in the hands

of the recipient. This is a horrid check proposed to be imposed on every taxable

person in the GST regime. In our view, the precondition relating to payment of

tax dues for allowing ITC in the hands of the recipient of goods/services is

slightly harsh, as it casts an additional burden on the recipient to prove that the

tax has been deposited by the supplier.

The matching of ITC may be better understood in the following steps:

Step 1: The Supplier supplies goods and/or services to the recipient.

for GST on GST Returns read along with the Model GST law, the matching,

reversal and reclaim of ITC can largely be understood as a fool proof

mechanism to tap revenue leakage in the hands of the Government. In order to

check for duplication of claim of ITC, the details of every inward supply

furnished by the taxable person (i.e. the “recipient” of goods and/or services) in

form GSTR-2 shall be matched:

With the corresponding details of outward supply furnished by the

corresponding taxable person (i.e. the “supplier” of goods and / or services)

in his valid return for the same tax period or any preceding tax period and

With the additional duty of customs i.e. IGST paid by the recipient in respect

of goods imported.

Therefore, the quintessential requirement for carrying out matching of ITC is

that the supplier must have filed his valid returns for the corresponding or

preceding tax period and/or the IGST has been paid by the recipient in case of

import of goods.

Failure to file valid return by the Supplier (or failure to pay appropriate IGST by

the recipient in case of import of goods) may lead to denial of ITC in the hands

of the recipient. This is a horrid check proposed to be imposed on every taxable

person in the GST regime. In our view, the precondition relating to payment of

tax dues for allowing ITC in the hands of the recipient of goods/services is

slightly harsh, as it casts an additional burden on the recipient to prove that the

tax has been deposited by the supplier.

The matching of ITC may be better understood in the following steps:

Step 1: The Supplier supplies goods and/or services to the recipient.

Step 2: The Supplier declares the details of outward supplies in his valid

return for the same tax period or preceding tax period and/or the recipient has

paid appropriate IGST in respect of import of goods.

Apparent contradictions:

In terms of the provisions of the Model GST law, for the purpose of

allowing ITC, a return may be considered to be a valid return only when

the appropriate GST has been paid in full by the taxable person as

shown in such return for a given tax period. Therefore, whether mere

filing of GSTR-1 (by 10th of the following month) without filing the relevant GSTR-3 (by 20th of the following month) for such tax period by the

Supplier can be considered as valid return?

If the answer to the above question is negative, then what is relevance of

the expression “….in his valid return” under Section 29(1)(a) of the

Model GST law, considering that the matching of ITC should take place

vis-à-vis valid return for a particular tax period?

The Model GST law provides that the ITC matching shall be carried out

for a tax period within the time prescribed. Therefore, it is open

for the Rules to provide whether the unmatched ITC must be

communicated either before filing of GSTR-3 or after filing of GSTR-3 by

the Recipient.

return for the same tax period or preceding tax period and/or the recipient has

paid appropriate IGST in respect of import of goods.

Apparent contradictions:

In terms of the provisions of the Model GST law, for the purpose of

allowing ITC, a return may be considered to be a valid return only when

the appropriate GST has been paid in full by the taxable person as

shown in such return for a given tax period. Therefore, whether mere

filing of GSTR-1 (by 10th of the following month) without filing the relevant GSTR-3 (by 20th of the following month) for such tax period by the

Supplier can be considered as valid return?

If the answer to the above question is negative, then what is relevance of

the expression “….in his valid return” under Section 29(1)(a) of the

Model GST law, considering that the matching of ITC should take place

vis-à-vis valid return for a particular tax period?

The Model GST law provides that the ITC matching shall be carried out

for a tax period within the time prescribed. Therefore, it is open

for the Rules to provide whether the unmatched ITC must be

communicated either before filing of GSTR-3 or after filing of GSTR-3 by

the Recipient.

Step 3: Upon filing of form GSTR-1 or GSTR-3 by the Supplier, as the case

may be, the details of outward supplies as filed by the Supplier shall flow as the

details of inward supplies of the Recipient in his GSTR-2 (i.e. auto-population of

details of ITC).

may be, the details of outward supplies as filed by the Supplier shall flow as the

details of inward supplies of the Recipient in his GSTR-2 (i.e. auto-population of

details of ITC).

Step 4: The Recipient shall verify, validate, modify or delete the auto-populated

details of ITC at the time of filing his GSTR-2 (by 15th of the following month)

after considering the clerical or non-clerical errors, including changes to be

made on account of issuance of Debit Notes.

It may be noted here that the recipient would be having a 5-day window

period where he can verify, validate, modify or delete the details of his

ITC, having cross reference to the details of outward supplies furnished

by his Supplier.

Further, in terms of the Business Process Report on GST Returns, a

responsibility is casted on the recipient to indicate the eligibility or noneligibility

of ITC in respect of each inward supply at the time of filing form

GSTR-2.

details of ITC at the time of filing his GSTR-2 (by 15th of the following month)

after considering the clerical or non-clerical errors, including changes to be

made on account of issuance of Debit Notes.

It may be noted here that the recipient would be having a 5-day window

period where he can verify, validate, modify or delete the details of his

ITC, having cross reference to the details of outward supplies furnished

by his Supplier.

Further, in terms of the Business Process Report on GST Returns, a

responsibility is casted on the recipient to indicate the eligibility or noneligibility

of ITC in respect of each inward supply at the time of filing form

GSTR-2.

Step 5: Assuming that form GSTR-1 of the recipient has already been filed

within the due date, the recipient shall ascertain the eligible ITC and upload the

details of every inward supplies in Form GSTR-2 within the due date.

within the due date, the recipient shall ascertain the eligible ITC and upload the

details of every inward supplies in Form GSTR-2 within the due date.

Step 6: The recipient shall ascertain the net GST liability after considering his

output tax liability on outward supplies made and eligible input tax credit

available on inward supplies. Such net GST liability would have to be

discharged by the recipient either using Electronic Cash or Credit Ledger (taking

into consideration the Rules for utilization of ITC). Consequent to which, the

recipient would be filing his GSTR-3.

It may be noted that in terms the provisions of Model GST law, in case

the taxable person has not furnished a valid return for the previous tax

period, he shall not be allowed to furnish the return for the current period. Further, a taxable person who has not furnished a valid return shall not

be allowed to utilize the ITC till he discharges the self-assessed tax

liability. Thus, in effect, the utilization of ITC for any given tax period is

always subject to furnishing of a “valid return” for pervious tax period by

such taxable person.

output tax liability on outward supplies made and eligible input tax credit

available on inward supplies. Such net GST liability would have to be

discharged by the recipient either using Electronic Cash or Credit Ledger (taking

into consideration the Rules for utilization of ITC). Consequent to which, the

recipient would be filing his GSTR-3.

It may be noted that in terms the provisions of Model GST law, in case

the taxable person has not furnished a valid return for the previous tax

period, he shall not be allowed to furnish the return for the current period. Further, a taxable person who has not furnished a valid return shall not

be allowed to utilize the ITC till he discharges the self-assessed tax

liability. Thus, in effect, the utilization of ITC for any given tax period is

always subject to furnishing of a “valid return” for pervious tax period by

such taxable person.

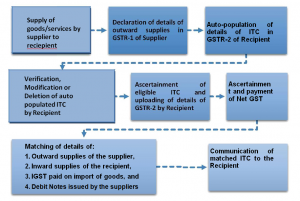

Step 7: The matching of details of outward supplies of the supplier and

corresponding details of inward supplies of the recipient, including IGST paid on

import of goods and Debit Notes issued by the suppliers shall be carried out at

system level.

In case the details match, then the ITC claimed by the recipient in his

valid returns shall be considered as finally accepted and such

acceptance shall be communicated to the recipient.

The question which arises here is whether the ITC as accepted above

can be considered as eligible credit for all practical purposes? The

answer to this lies in Section 29(2) of the Model GST law, which states

that “…., subject to the provision of Section 16, ….”. Thus, the

matched ITC which is finally accepted is only for the limited purpose of

system matching, which can always be subject to manual scrutiny at later

point of time.

The concept of ITC matching is depicted in the form of a flowchart hereunder (From Recipient‟s Perspective):

corresponding details of inward supplies of the recipient, including IGST paid on

import of goods and Debit Notes issued by the suppliers shall be carried out at

system level.

In case the details match, then the ITC claimed by the recipient in his

valid returns shall be considered as finally accepted and such

acceptance shall be communicated to the recipient.

The question which arises here is whether the ITC as accepted above

can be considered as eligible credit for all practical purposes? The

answer to this lies in Section 29(2) of the Model GST law, which states

that “…., subject to the provision of Section 16, ….”. Thus, the

matched ITC which is finally accepted is only for the limited purpose of

system matching, which can always be subject to manual scrutiny at later

point of time.

The concept of ITC matching is depicted in the form of a flowchart hereunder (From Recipient‟s Perspective):

Reversal of ITC / Mismatch of ITCIn terms of the provisions of Model GST law, the reversal of ITC arises when:

Reversal of ITC / Mismatch of ITCIn terms of the provisions of Model GST law, the reversal of ITC arises when:- there is excess claim of ITC by the recipient as against the tax declared by

the supplier, or - the outward supply is not declared by the Supplier, or

- there is a duplication of claim of ITC by the recipient.

Excess claim of ITC

In case the ITC claimed by the recipient is in excess of the tax declared by the

supplier or where the details of outward supply are not declared by the supplier

in his valid returns, the discrepancy shall be communicated to both the supplier

and the recipient. Similarly, in case, there is duplication of claim of ITC, the

same shall be communicated to the recipient. It may be noted that in case the

ITC claimed by the recipient is less than the tax declared by the supplier, there

may not be any communications to either Supplier or the recipient.

The Supplier will be asked to rectify the discrepancy of excess claim of ITC and

in case the Supplier has not rectified the discrepancy communicated in his valid

returns for the month in which discrepancy is communicated then such excess

ITC as claimed by the recipient shall be added to the output tax liability of the

recipient in the succeeding month. Such excess ITC claimed is added back to

output tax liability of the recipient could be for the reason that the Supplier can

issue Debit Note only when the value and/or tax as shown in the tax invoice is

less than the taxable value and/or tax in respect of supply of goods and/or

services. Issuance of Debit Note by the supplier nullifies the effect of excess

availment of ITC by the supplier. Similarly, duplication of ITC claimed by the

recipient shall be added to the output tax liability of the recipient in the month in

which such duplication is communicated.

The recipient shall be liable to pay interest on the excess or duplicate ITC

added back to the output tax liability of the recipient from the date of availing of

ITC till the corresponding additions are made in their returns. In GST regime,

the reversal of ITC refers to adding back either the excess claim of ITC or

duplication of ITC to the output tax liability of the recipient. Thus, the person

who claims the excess ITC shall have bear to brunt of Interest till such excess

ITC is accepted at system level.

In case the ITC claimed by the recipient is in excess of the tax declared by the

supplier or where the details of outward supply are not declared by the supplier

in his valid returns, the discrepancy shall be communicated to both the supplier

and the recipient. Similarly, in case, there is duplication of claim of ITC, the

same shall be communicated to the recipient. It may be noted that in case the

ITC claimed by the recipient is less than the tax declared by the supplier, there

may not be any communications to either Supplier or the recipient.

The Supplier will be asked to rectify the discrepancy of excess claim of ITC and

in case the Supplier has not rectified the discrepancy communicated in his valid

returns for the month in which discrepancy is communicated then such excess

ITC as claimed by the recipient shall be added to the output tax liability of the

recipient in the succeeding month. Such excess ITC claimed is added back to

output tax liability of the recipient could be for the reason that the Supplier can

issue Debit Note only when the value and/or tax as shown in the tax invoice is

less than the taxable value and/or tax in respect of supply of goods and/or

services. Issuance of Debit Note by the supplier nullifies the effect of excess

availment of ITC by the supplier. Similarly, duplication of ITC claimed by the

recipient shall be added to the output tax liability of the recipient in the month in

which such duplication is communicated.

The recipient shall be liable to pay interest on the excess or duplicate ITC

added back to the output tax liability of the recipient from the date of availing of

ITC till the corresponding additions are made in their returns. In GST regime,

the reversal of ITC refers to adding back either the excess claim of ITC or

duplication of ITC to the output tax liability of the recipient. Thus, the person

who claims the excess ITC shall have bear to brunt of Interest till such excess

ITC is accepted at system level.

Re-claim of ITC

Re-claim of ITC refers to taking back the ITC reversed in the Electronic Credit

Ledger of the recipient by way of reducing the output tax liability. Such re-claim

can be made by the supplier only in case the supplier declares the details of

invoice and/or Debit Notes in his valid return within the prescribed timeframe. In

such case, the interest paid by the recipient shall be refunded to him by way of

crediting the amount to his Electronic Cash Ledger.

However, it may be noted that no refund of interest would arise in case the

excess ITC reversed was on account of duplication of ITC claim, as the same

would be considered to be contravention of the GST provisions, where refund is

allowable.

Compliance Rating under GST

GST proposes to bring in a new system of compliance rating score for every

taxable person, based on the record of compliance with provisions of law. This

score shall be determined on the basis of certain parameters such as timely

furnishing of returns, accuracy of data furnished, timely payment of taxes, etc.

The GST compliance rating score is somewhat similar to the concept of the

Denied Entities List (DEL, earlier called „Black List‟) under the provision of Rule

7 of the Foreign Trade (Regulation) Rules, 1993, wherein a total of 14

conditions have been described for invocation DEL before a company can be

refused a license by the Directorate General of Foreign Trade.

The GST compliance rating score shall be updated at periodic intervals and

intimated to the taxable person and also placed in the public domain. A

prospective customer/client can view his supplier‟s GST compliance rating

score and take appropriate decisions whether to deal with a particular supplier

or not. It is therefore important for every taxable person to ensure adequate

level of compliance, which will not only facilitate ease of doing his business, buy

will also have a bearing on his reputation.

“Success will lead your way, if you develop a passion

Re-claim of ITC refers to taking back the ITC reversed in the Electronic Credit

Ledger of the recipient by way of reducing the output tax liability. Such re-claim

can be made by the supplier only in case the supplier declares the details of

invoice and/or Debit Notes in his valid return within the prescribed timeframe. In

such case, the interest paid by the recipient shall be refunded to him by way of

crediting the amount to his Electronic Cash Ledger.

However, it may be noted that no refund of interest would arise in case the

excess ITC reversed was on account of duplication of ITC claim, as the same

would be considered to be contravention of the GST provisions, where refund is

allowable.

Compliance Rating under GST

GST proposes to bring in a new system of compliance rating score for every

taxable person, based on the record of compliance with provisions of law. This

score shall be determined on the basis of certain parameters such as timely

furnishing of returns, accuracy of data furnished, timely payment of taxes, etc.

The GST compliance rating score is somewhat similar to the concept of the

Denied Entities List (DEL, earlier called „Black List‟) under the provision of Rule

7 of the Foreign Trade (Regulation) Rules, 1993, wherein a total of 14

conditions have been described for invocation DEL before a company can be

refused a license by the Directorate General of Foreign Trade.

The GST compliance rating score shall be updated at periodic intervals and

intimated to the taxable person and also placed in the public domain. A

prospective customer/client can view his supplier‟s GST compliance rating

score and take appropriate decisions whether to deal with a particular supplier

or not. It is therefore important for every taxable person to ensure adequate

level of compliance, which will not only facilitate ease of doing his business, buy

will also have a bearing on his reputation.

“Success will lead your way, if you develop a passion

This article was written by CA Ronak Agarwal in his personal capacity. The opinions/facts/information expressed in this article is the author’s own and do not reflect the view of the aapkaconsultant.com.